Banking Reimagined:

How generative AI reshapes the customer banking journey

10.30.2024 | By: Charles Moldow, Nico Stainfeld, Tireni Ajilore

Special thanks to our summer research associate, Tireni Ajilore, for leading research and writing efforts for this series.

Banks today struggle with two seemingly incompatible realities: stubbornly low customer satisfaction and high service costs. They’ve invested massive amounts of time and capital in technology to help. Has it worked? Will it?

Traditional AI has delivered enormous value to banks in areas like credit scoring, fraud detection, and risk management. Yet, while predictive models excel in handling structured data and repetitive tasks, they struggle when confronted with unstructured and less predictable scenarios—essentially, the human elements of banking.

This is where generative AI comes in. Unlike predecessor technologies, generative AI doesn’t just predict outcomes based on past patterns. It can process unstructured data, engage with customers in real time, and deliver personalized experiences that traditional AI cannot.

In many ways, generative AI isn’t just another tool—it represents a fundamental shift in how financial institutions can approach customer interaction, operational efficiency, and even core elements of their business strategy like underwriting. Generative AI has the potential to make banking more efficient, more personalized, and, ultimately, more human.

Based on our research and conversations with 20 banking executives across business, compliance, product and AI research, this series of posts examines how generative AI can plug into every phase of the consumer and retail banking lifecycle, and identifies strategic opportunities for both incumbents and startups to harness its potential.

Today, we’ll present a high-level overview, covering everything from customer acquisition to onboarding, engagement, and collections. In the coming weeks, we’ll take a closer look at each stage, culminating with a market map of key startups in the space.

Where incumbents and startups can leverage generative AI

Generative AI presents a transformative opportunity for both incumbent banks and fintech startups—but how these two groups leverage this technology will differ in key ways.

For incumbents: Building on existing strengths

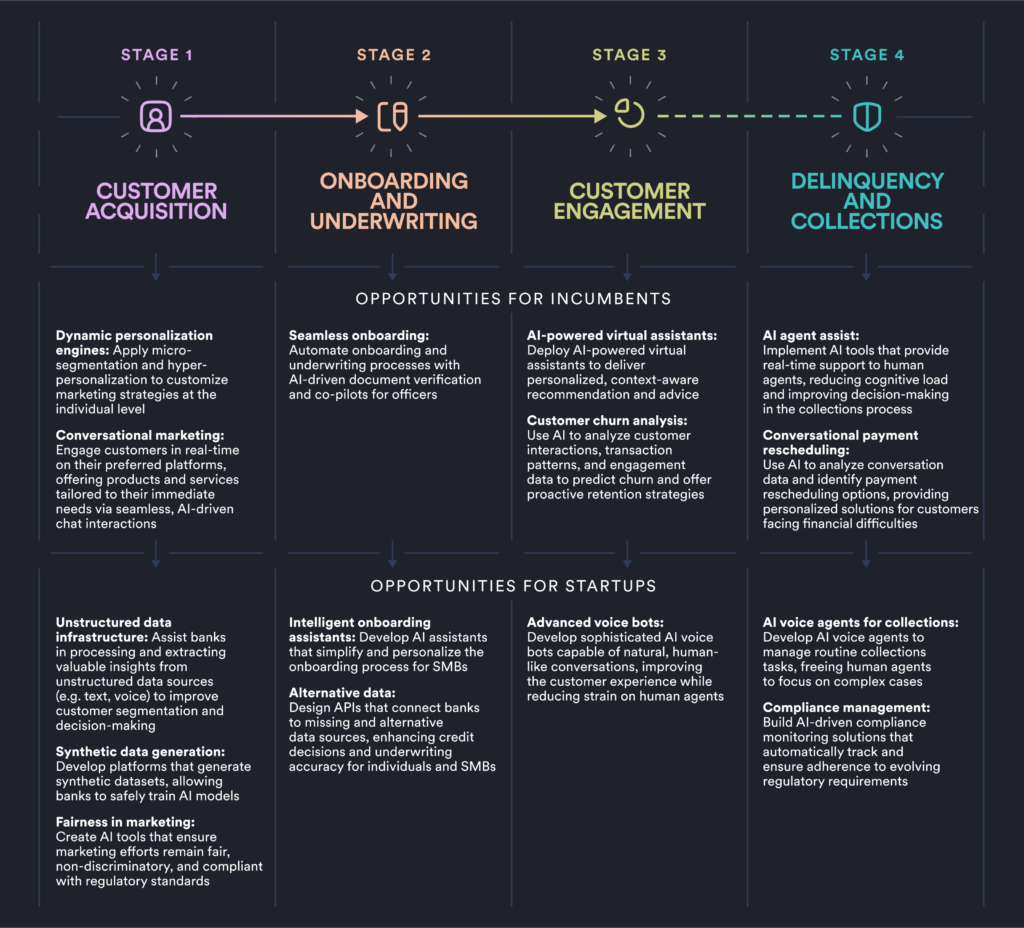

Incumbent banks have a distinct advantage: vast amounts of data and a large, loyal customer base. The challenge lies in fully utilizing these resources. Generative AI offers a path forward. By integrating generative AI into their existing systems, incumbents can both improve operational efficiency and deliver richer, more personalized experiences that keep customers loyal and engaged.

- Personalization engines that truly understand your customers: Traditional AI models rely heavily on structured data, which limits their understanding of customer needs. By contrast, generative AI can analyze and act on unstructured data, such as call transcripts and social media interactions. This allows banks to build more comprehensive customer profiles and offer tailored products that enhance satisfaction and retention.

- Streamlined onboarding and underwriting workflows: Banking is rife with tedious, manual tasks that slow down both employees and customers. With generative AI, processes like document verification and compliance reviews can be automated, reducing bottlenecks and making interactions smoother for everyone involved. This not only improves efficiency but frees up human resources for higher-value tasks.

- Smarter virtual assistants for better customer engagement: Today’s customers expect more than transactional banking services—they want personalized advice and real-time support. Generative AI enables banks to deploy advanced virtual assistants that offer tailored financial guidance and help customers navigate complex decisions. This deepens engagement and strengthens the bank-customer relationship, which can drive profitability in the long run.

- Real-time agent support in collections and customer service: Managing customer service, particularly on delinquent accounts, is a costly and complex process for banks. Generative AI can support collections agents by offering real-time guidance, suggesting personalized payment solutions, and ensuring compliance with regulatory frameworks. This improves the customer experience while reducing risk and improving the bank’s ability to recover revenue efficiently.

There is a vast amount of value generative AI can deliver to incumbent banks. But currently, most of it hasn’t been unlocked due to the regulations and complex processes required to operate these financial institutions. This creates an opportunity for startups.

For startups: Capitalizing on gaps in legacy systems

While incumbent banks have the advantage of scale and established infrastructure, they are often slowed by legacy systems that limit their ability to fully embrace generative AI. This is where startups have a unique advantage. With no legacy constraints, fintech startups can build nimble, AI-native solutions that address inefficiencies in traditional banking models and offer entirely new customer experiences.

- Building infrastructure for unstructured data: Roughly 80% of banking data is unstructured—ranging from emails to chat logs to customer inquiries. Traditional AI models can’t process this type of data effectively. Startups can develop tools that help banks unlock the value of unstructured data, offering new insights into customer behavior and allowing for highly personalized services.

- Creating synthetic data for safe innovation: Privacy regulations make accessing high-quality data for training AI models a significant challenge. Startups can help by developing platforms that generate synthetic data—artificial datasets that closely mimic real data without compromising privacy. These platforms enable banks to train and test AI models without compromising sensitive information, accelerating innovation in a highly regulated environment.

- Automating onboarding with AI-powered assistants: Speed and personalization are crucial in customer acquisition, particularly when it comes to onboarding. Startups can automate complex processes like SMB loan origination, making them faster, more efficient, and more personalized. This leads to higher conversion rates, lower customer churn, and increased satisfaction.

- AI for compliance management: The regulatory environment in banking is complex and constantly evolving, making compliance a costly and time-consuming task. Startups can build AI tools that monitor compliance in real time, flagging potential issues before they escalate into costly penalties. This proactive approach not only reduces regulatory risk but also allows banks to operate more efficiently and focus resources on innovation and growth.

Startups can scratch an itch that’s just out of reach for many incumbent financial institutions. Building AI-first solutions gives startups an opportunity to create value in between the legacy systems slowing incumbents down.

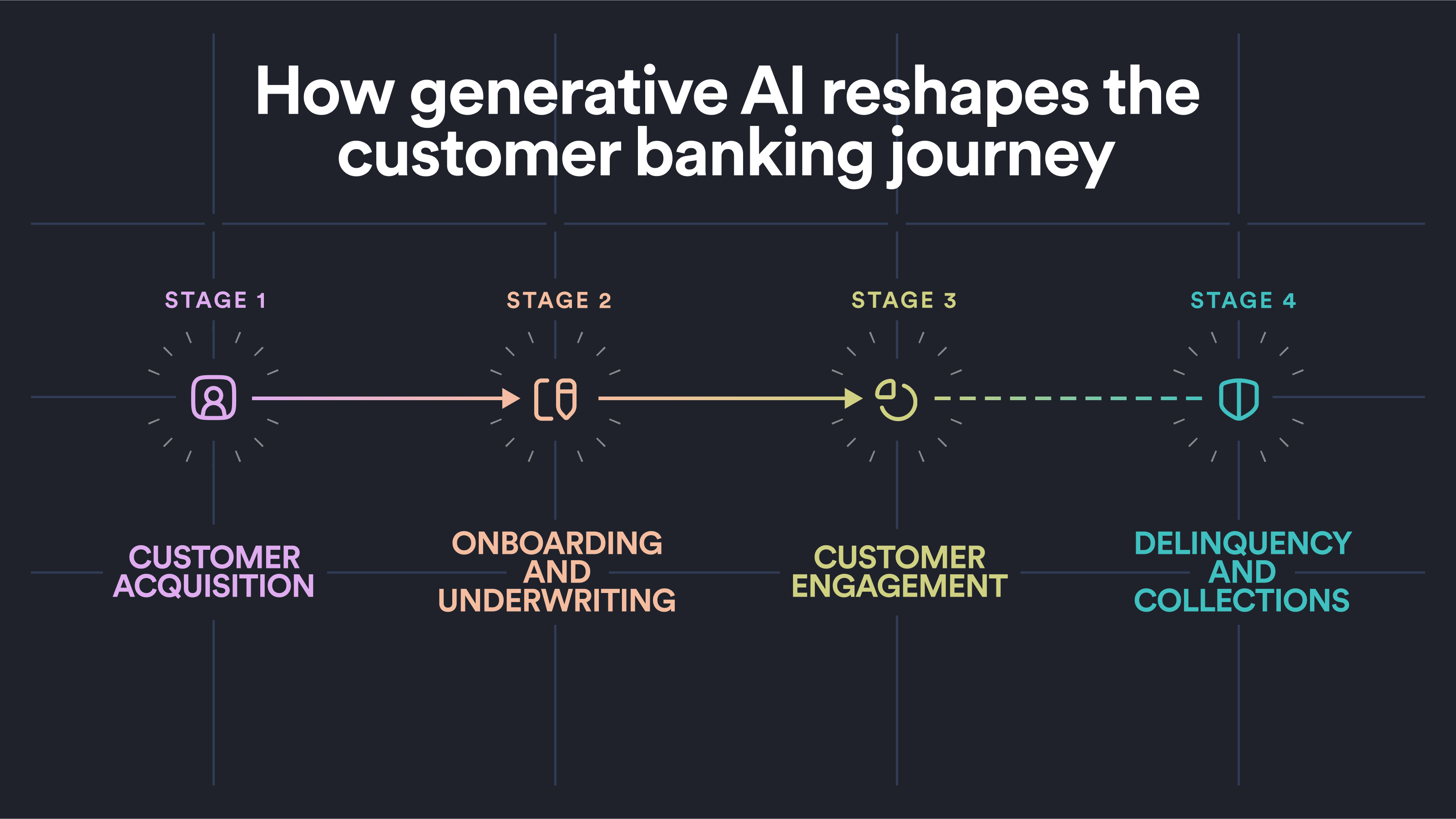

How generative AI plugs into each stage of the customer banking journey

To grasp the transformative potential of generative AI, it’s essential to understand the banking lifecycle and how this technology integrates with it. Generative AI offers unique opportunities at every stage—enhancing customer experiences, improving operational efficiency, and ultimately boosting profitability.

In the sections that follow, we’ll explore each phase of the banking lifecycle, examining how generative AI is poised to transform customer acquisition, onboarding and underwriting, customer engagement, and the sensitive realm of delinquency and collections. We’ll outline the opportunities for both incumbent banks and fintech startups at each stage.

Here’s an overview:

Published on October 30, 2024

Written by Foundation Capital