If you’re building in fintech and don’t consider implementing blockchain infrastructure somewhere in the stack, you’re missing out.

At Foundation, we believe the integration of blockchain rails into fintech applications is the catalyst for mainstream crypto adoption. Once a standalone technology, crypto is now becoming part of everything financial. If we do our jobs right, blockchain-powered applications will soon be in everyone’s pocket, whether users know it or not. This is a very exciting time for Foundation: We’ve been investing in both fintech and crypto for 10+ years now, and the intersection is going to be even more interesting.

Crypto-native innovation is coming on strong. As these new economic levers enter fintech, the opportunity for platform disruption is huge. Novel business models are emerging as new monetization and incentive mechanisms are built directly into web2 UIs. The way we think about capital formation and consumption is changing too, with alternative funding mechanisms such as token launches and equity tokens democratizing access to funding. Products built on the blockchain will become cheaper to operate, forcing incumbent players to innovate or be driven obsolete by pricing competition. Companies leveraging blockchain technology are also inherently global and composable from day one, so TAM is not constrained by currency, local infrastructure or siloed systems of record.

What brought crypto out of the shadows?

The convergence of fintech and crypto wasn’t obvious. The history of these two sectors reads like a tale of two cities.

On one hand, we saw a real transformation of financial services over the past 10-15 years (i.e. fintech). Banking went mobile, followed by similar trends across wealth management, insurance, taxes, accounting, and more. Accessibility, clean UI and mass distribution became table stakes. At the same time, crypto emerged as an alternative for degens and haters of the current financial systems. We had two new technologies, but they existed for different users, with what seemed like opposing ideologies.

Over time — and perhaps to the chagrin of both extremes — crypto professionalized, paving the way for blockchain tech to be embedded in fintech apps. It’s worth noting three major factors that brought us to this point:

Development of enterprise-grade infrastructure (L1s), along with custodial and risk products. High-throughput L1s like Solana (where Foundation was the first venture investor) now meet the performance standards to deploy fully on-chain financial infrastructure. Purpose-built projects like the Canton Network are providing institutions privacy and more business-friendly use cases. Custody providers like Fireblocks and Ledger have gained enterprise trust. And blockchain analytics platforms like TRM Labs and Chainalysis have amassed powerful historical datasets to aid in blacklisting bad actors and providing more robust monitoring.

Key crypto legislation around definition, permitted use, and accounting of digital assets, namely the CLARITY and GENIUS acts, have put Washington’s stamp of legitimacy on the crypto sector. While votes are ongoing, the legislation has baseline support from both parties. Pushback from traditional depository institutions (and now Tether, too - though are we really that surprised?) is actually a compliment: it reflects the real threat yield-bearing stablecoins pose to the sector’s profitability.

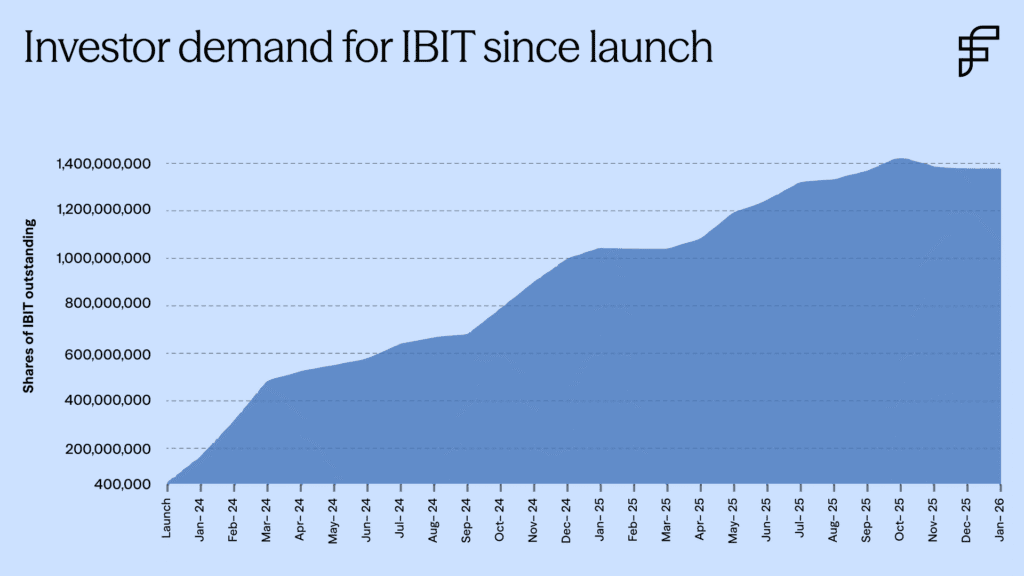

The successful launch and growth of tokenized money market funds (TMMFs), crypto ETFs, and tokenized private credit funds was a stamp of approval from the biggest normies of all: incumbent financial institutions. BlackRock’s IBIT was dubbed one of the greatest ETF launches in history and has since grown to over $50B in market cap. Circle’s USYC TMMF sits at a $1.5B market cap less than 6 months after launch, now rivaling BlackRock’s BUIDL, also launched in 2025. Meanwhile, Apollo is actively bringing private credit on-chain, teaming up with Solana and Kamino (another FC portco!), alongside Securitize and a host of other crypto firms, to launch ACRED last year.

Where can fintech founders build with crypto?

Now that blockchain infrastructure is deemed legitimate, builders across financial services must ask themselves where it makes sense to implement the technology — and then actually build with it. So, where might blockchain collide with fintech at an infrastructure level today?

Lending and credit:

Post-ZIRP, balance sheet businesses gained a somewhat unfair bad rep thanks to low-tech, capital intensive business models. UX continues to improve, but these companies are in need of deeper transformation. Incorporating blockchain technology — at the point of underwriting and decisioning, as a capital provider, or for payment facilitation — can reduce upfront capital outlay, improve operating margins and decrease delinquencies. Kamino, for instance, offers access to isolated lending markets and a suite of lending products that give institutions new avenues for borrowing.

Capital markets:

This is similar to lending but not constrained to credit needs. Here we’ve seen short-term success from platforms like pump.fun, but examples such as Dupe’s launch of $DUPE on Solana and MIRA’s raise for cancer research show what’s truly possible with on-chain capital markets. Projects like Echo also are making traditional private investing available to a broader user base via the tokenization (more on this later) of equity or equity-like assets.

There are different venues in which this capital formation can happen; our partners Rodolfo and Alejandra have written about about how Solana is well positioned to serve companies building in this space.

Trading (clearing and settlement):

The optimal trading environment is programmable, continuous, low cost, and high throughput. Crypto markets have been 24/7 for years and allow for simpler global trading. An L1 like Solana is the ideal trading venue from a money movement perspective. In addition, the creation of multiple concurrent leaders on Solana would theoretically allow people closest to market-moving events to land trades the fastest, creating a more level playing field.

As we’ve seen via recent announcements from NYSE and NASDAQ, blockchain infrastructure is becoming synonymous with cutting-edge technology in the traditional equities arena. Our portfolio company Helius now offers advanced market structure products ranging from low-latency feeds to bespoke high-bandwidth connections.

DoubleZero, another recent Foundation investment, is building a dedicated, high-performance network layer to further reduce congestion issues and create a "fast lane" for blockchain traffic.

Payment rails:

Last year, we wrote about how stablecoins are rewriting the way money moves.Traditionally, consumers and businesses have had to choose between cheap but localized (PIX, UPI, FedNow) or expensive and slow but global (SWIFT) payments. Credit card networks sit somewhere in between, with most of the cost eaten by the merchant as opposed to the card user.

With stablecoins, the opportunity to build flexible, global, and high-volume payments products is blown wide open. BCB Group, a 2022 Foundation investment, has been enabling financial institutions and startups to partake in this new transaction economy since before it was cool.

We’d also be remiss not to mention the role stablecoins will play in the emerging agentic transaction economy. Microtransactions between agents around the globe will demand low-cost infra, 24/7 rails, and an agnostic currency. The team at our portco ATXP is tackling this new frontier.

Custody of funds:

Between scale-ups going after bank charters directly and the increasing acceptance of stable-denominated wallets as a means of value storage, seeking bank sponsorship is no longer a requirement for builders (and BaaS is essentially out of the question). Crypto wallets enable seamless money movement and yield opportunities, which generates additional monetization levers. Our friends at Brale (yep, another Foundation portfolio company) are enabling the issuance, custody and movement of stables across web2 and web3 applications, providing an excellent real world example of crypto-fintech convergence.

Tokenization of assets:

Tokenization is about bringing any analog unit of value — dollars, bank deposits, equities, commodities, Pokemon cards — “on-chain” with a digital representation. Tokenizing assets will become increasingly lucrative as 1) infrastructure bridging the “analog” and “digital” matures and 2) traditional finance becomes more programmable and composable.

For example, gaining exposure to metals was previously an arduous task for retail traders, but we’re entering a new paradigm. Activity on perp platforms like Hyperliquid’s HIP-3 hit $5B+ daily volume in early Feb and now accounts for 2% of global silver trading. In addition, tokenization of US equities enables global access to blue chip assets, without the need for a US brokerage account.

What new platforms will be built?

As this hybrid approach to building becomes table stakes, new experiences will change what users expect from their financial service providers. Here’s what we expect to see:

The expansion of risk-adjusted, yield-bearing accounts, resulting in the overhaul of <0.50% APY vehicles offered by traditional financial institutions. Automated yield farming, made possible by companies like YO (a recent Foundation investment), will transform treasury management, high-yield savings and checking, money market funds, and more.

Truly hybrid, full-stack banking experiences offering a myriad of financial services on and off-chain. These platforms won’t just serve existing crypto adopters but normies, too. Traditional institutions will implement blockchain technology across the org — not shoehorned by niche digital assets teams — with the help of infrastructure providers like our portfolio company Omnia. We’ll also see entirely new wealth platforms building at this intersection from day one.

Predatory, opaque lending schemes (both consumer and B2B) will become obsolete as blockchain integration forces transparency and efficiency. Automation via smart contracts and an abundance of global liquidity make DeFi lending ripe for web2 deployment, either as a standalone product or an embedded experience in platforms with existing distribution. However, we need more robust credit scoring mechanisms and intuitive on-ramping infrastructure before we can expect real disruption.

On-chain trading becomes the default and ushers in a new wave of participants. As the amount of assets represented on-chain grows, investing and trading will become increasingly relevant to non-crypto users. While the prospect of yield is an okay carrot, we believe that the ability to trade traditional instruments (equities, commodities, FX) will be the killer use case that brings net-new customers on-chain. Imagine buying gold, private shares, Pokemon cards, and Nvidia stock on the same platform.

Meaningful expansion of TMMF’s share as a percentage of total MMF AUM as institutions adopt on-chain trading technology and existing repo infrastructure becomes obsolete. TMMFs are more efficient than their traditional banking equivalents, with public blockchains making MMFs faster and perhaps even commanding higher yield. While TMMFs are becoming one of the first “mainstream” use cases for blockchain adoption within FIs, AUM accounts for well under 1% of the $8T held in traditional MMFs today. Expansion here represents a $15B+ revenue opportunity (based on <20 BP management fee).

The scope of crypto’s quiet mainstream integration makes it nearly impossible to present an exhaustive list. Still, the ideas above should give you a feel for its massive, and now seemingly inevitable, role in disrupting the financial order at retail and institutional levels.

Where does Foundation Capital fit in?

We've been investing at the intersection of fintech and crypto for more than a decade, patiently waiting for these two worlds to collide! At Foundation, we’ve always believed that the most interesting opportunities live not in one world or another, but at the seams between them. We're in the midst of the quiet crypto integration, and we can't emphasize this enough: if you don't get smart on building with blockchain infrastructure, you're going to get left behind.

Of course, if you’re already building at and for the seams, we want to talk to you! There’s no better time to disrupt the status quo, and we’re excited to get to work.