$100M in ARR is the best north star for startup success. Here’s how founders can get there.

02.24.2024 | By: Ashu Garg

Photo credit: yosuke muroya

I revisit the storied “unicorn” status, now a decade old. I propose a more rigorous benchmark for startup success, $100M in ARR, and outline the concrete steps that founders can take to reach it.

Reflections on the “unicorn,” 10 years in

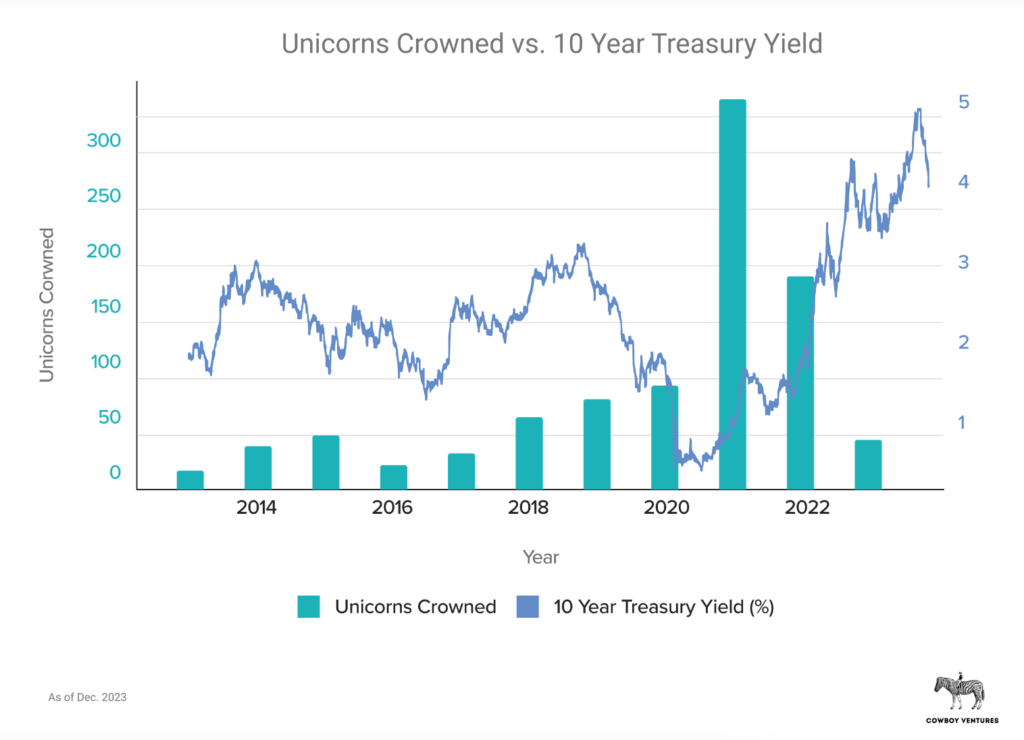

Ten years ago, Cowboy Ventures introduced the term “unicorn” to describe U.S.-based startups valued at over $1 billion. At the time, only 39 companies—a mere 0.07% of venture-backed startups—had reached this valuation, making the unicorn a near-mythical achievement. Last month, Cowboy updated their landmark report, providing a chance for readers to reassess what a $1 billion valuation means today.

There are 532 unicorns today—a 14x increase since 2013. This comes as no surprise to those in the tech industry. Fueled by a 13-year bull market and a surge in venture capital funding, software valuations have soared.

Consider the math: in 2021, the average multiple for a top 100 private cloud company was 34x. This fell to 30x in 2022 and dropped further to 26x in 2023. Yet, even at a 26x multiple, a startup only needs $36M in ARR to be crowned a unicorn. As investors found ways to rationalize these multiples, what once was a symbol of extraordinary achievement has become markedly less so.

Source: Cowboy Ventures 2024 report

As a result, the “unicorn” label has lost much of its original meaning. Its allure has distracted many founders from what really matters: building an enduring business.

In what follows, I draw out three key insights from Cowboy’s updated analysis and share my perspective on the path to building a startup that can grow into a generationally important company.

Takeaway 1: The unicorn herd is set to thin

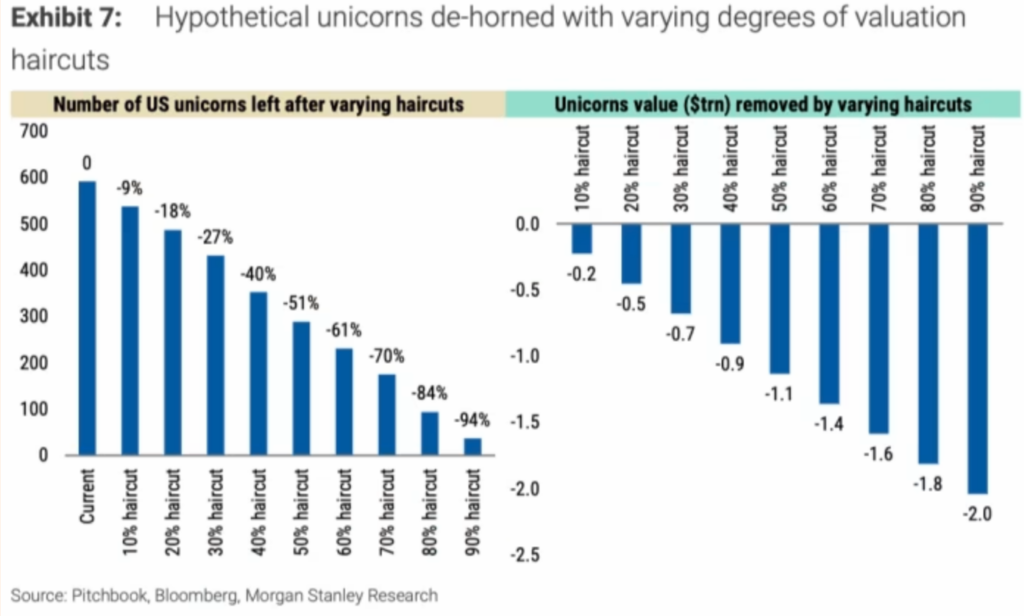

In the coming years, Cowboy predicts a marked reduction in the number of unicorns. By their estimate, the herd will dwindle to around 350: about two-thirds of its current size. Morgan Stanley’s research forecasts a more drastic decrease based on secondary transaction prices, which suggest that startup valuations will fall by half. This would reduce the unicorn population by 51%, erasing around $1.1T in value.

Source: The Financial Times

In some cases, these corrections reflect a change in multiples, which in the grand scheme of things, is a speed bump. In many other cases, the startups don’t have a path to delivering venture-scale returns and have no alternative but to shut down. The sudden demise of once-celebrated unicorns like Convoy (valued at $3.8B in 2022), Olive AI (valued at $4B in 2021), and Veev (valued at $1B in 2022) is just the beginning.

More broadly, investors are beginning to realize that gross margins matter, transactional revenue is worth a fraction of recurring revenue, and many sectors of the economy are just not a good fit for the venture model. This issue goes beyond unicorns. 3,200 private VC-backed U.S. companies shut down in 2023: a 50% increase from 2022, and a 300% rise since 2019. Q3 of 2023 alone saw startup closures climb to 4x the average rate.

2024 will likely be another year of reckoning for venture, as we continue to work through the excesses of the ZIRP era. While extremely trying, this process will allow entrepreneurs to once again focus fully on what should be their core mission: building innovative and resilient businesses.

Takeaway 2: Startup value now lies firmly enterprise

Cowboy’s analysis surfaces another notable finding: the locus of startup value has shifted stanchly to enterprise. In 2013, consumer startups made up 62% of the unicorn cohort and were responsible for 80% of its total value. Today, the scenario has flipped: enterprise unicorns number 416, representing 78% of the total unicorn population. Their collective valuation stands at $1.2T, accounting for 80% of all unicorn value.

This shift to enterprise is driven first and foremost by the scale of the opportunity. Enterprises spend $5T (yes, trillion) annually on IT, and this market is experiencing multiple disruptions, including the shift to cloud, the rise of digital assets, and the growing severity of security threats. This creates a massive opportunity for startups. Public market investors have also come to appreciate the compounding power of the SaaS business model and are rewarding these companies with higher multiples.

In my opinion, enterprise software will continue to dominate value creation in the venture ecosystem, especially as AI drives a new multi-decade cycle of innovation and automation across industries.

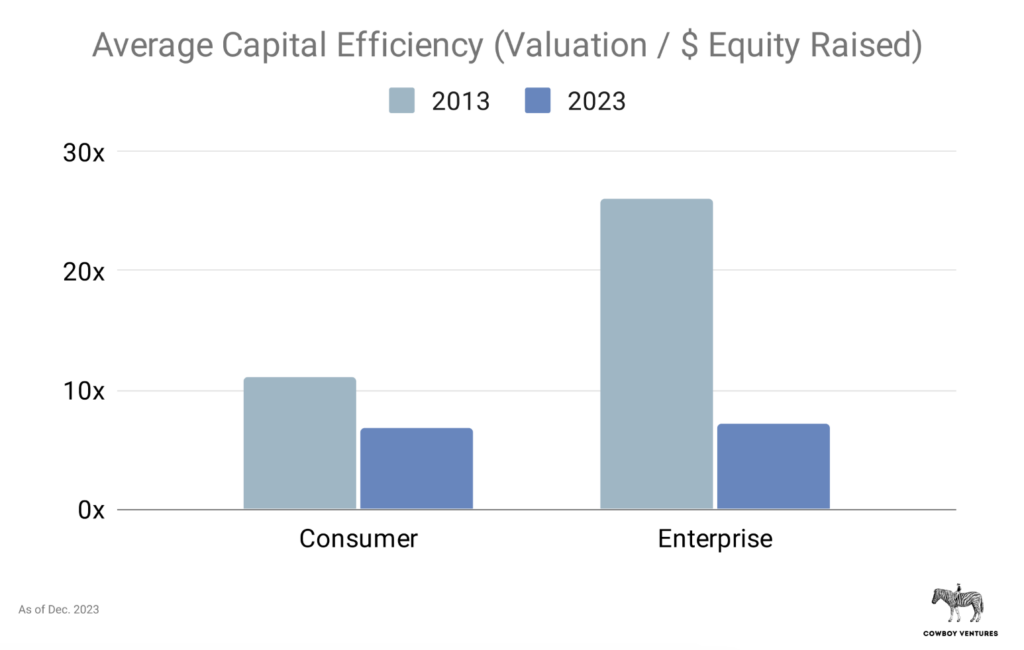

Takeaway 3: Capital efficiency has declined

Over the past decade, the capital efficiency of enterprise startups (as measured by a startup’s valuation divided by the equity capital it’s raised) has plummeted from an impressive 26x to just 7x. This number is likely overstated given the inflated valuations.

Source: Cowboy Ventures 2024 report

The sense that money was “free” likely contributed to this decline. Another contributing factor was the focus on growth at all costs. Investor FOMO didn’t help, and we’re still seeing that today with distorted valuations for all things “AI.”

$100M in ARR: A better benchmark for startup success—and how founders can get there

During this turbulent transition, my rallying cry for enterprise founders is to focus on becoming “centaurs”: a term for startups that hit $100M in ARR. At this stage, an enterprise software startup is default alive and typically able to grow ~30% while staying cash flow positive. Also, given the scale of enterprise IT spend, most centaurs have a plausible path to being enduring public companies and, over time, becoming real unicorns: companies with $1B in ARR!

So what does it take to get to $100M in ARR? Let’s break the journey into three distinct phases.

Phase 1: $0–1M in ARR

The first step is perhaps the hardest. Going from an idea to the first $1M in ARR often requires convincing customers to bet their jobs or even their careers on something completely unproven. As the adage goes, no one gets fired for buying IBM!

The keys at this stage are:

- Crisply define the problem you’re solving: Founders typically start with a broad problem and a vision to change the world. Its critical to go beyond that to identify an acute pain point that you believe you can solve in the near term.

- Identify your ideal customer profile, or ICP: This is the persona who’s feeling the most acute pain from the problem above.

- Build a Minimum Saleable Product, or MSP: An MSP is not only “viable” but also polished and comprehensive enough for customers to invest in and integrate into their operations. This could involve meeting compliance and uptime requirements, or perhaps providing enterprise-grade customer support.

To achieve these goals, finding a “wedge” is essential. This means narrowing your product’s focus so that it solves a specific pain point for your ICP dramatically better than the alternatives. Guiding your customers through the onboarding process is also crucial. This ensures that they not only successfully adopt your product, but become heroes in their organizations for doing so.

To quote another adage, don’t sell software, sell promotions! This means shifting your focus from selling features and technical capabilities to selling the value and outcomes that your product provides.

Having seen more than 50 companies attempt to cross this threshold firsthand, I’ve yet to come across a company that failed to do so because of weak technical chops or market conditions. At this stage, startups almost always fail due to founder conflict, an inability to hone in on a value prop that is compelling enough for customers to make the leap of faith, or because the cost of onboarding the technology (the time to set up, configure, and train users) outweighs its perceived value.

Phase 2: $1–10M in ARR

Once they pass the $1M ARR mark, most startups have concrete proof of market demand and initial feedback from customers about the value their product delivers. These early adopters often have the right combination of sophistication and passion to help founders define their broader product roadmap.

To reach $10M in ARR, a startup needs to accomplish three core tasks:

- Develop a scalable demand generation engine: This involves implementing a systematic strategy to identify, attract, and engage with prospects. There’s a whole suite of tools that startups can use here, ranging from events and conferences to content marketing and paid media. The key is to figure out what formula works for your startup. On this front, I see varied strategies succeed depending on the market, the nature of the product, the target ICP, and the founder’s DNA.

- Shift from founder-based selling to a structured sales team: This entails recruiting around a dozen salespeople and enabling them so that they deeply understand the product’s value prop, communicate it effectively to potential buyers, and get customers to the finish line.

- Demonstrate the value created for customers in order to drive renewals: Ensuring that customers get value from the product is necessary but not sufficient to ensure renewals. Often, customers need ROI studies, manager dashboards, and other tools to make the case for budget internally. While all of this is easier than the initial sale, founders are best served by treating renewals like new sales and putting similar energy behind them, especially in the early days.

The most critical hire at this stage is the VP of Sales. If you hire the wrong person, you’ll likely lose a year. Depending on your cash situation, you may not recover from this setback. The ideal candidate is someone who has a track record of success at an equivalent-stage company, selling to a comparable ICP at an analogous price point (ACV) with a similar sales cycle. This person should also be a “player-coach,” capable of leading from the front and closing deals while also being able to hire and manage a small team.

The most common mistake at this stage is hiring salespeople before building a sufficient sales pipeline. With the right compensation plan, skilled salespeople will stretch and close more than their quota capacity suggests. However, without enough leads, the best salespeople will likely leave first, creating a vicious spiral of turnover. In real estate, they say it’s all about location, location, location. At this stage in enterprise software, it’s all about pipeline, pipeline, pipeline!

Phase 3: $10-100M in ARR

Once you hit $10M in ARR, you likely have more than 50 customers, a clear sales process, a proven approach to hiring and enabling AEs, and a repeatable strategy for generating demand.

Until the $10M milestone, most startups have player-coaches leading each function and very lightweight processes. While it’s important for founders to remain hands-on and not overly delegate, scaling further requires investing the time and energy to hire the right leaders for each function and establish strong management processes.

Operational complexity increases exponentially at this stage, causing communication and coordination challenges like the “telephone game” to arise. A frequent frustration the founders voice is “I’ve doubled the team and yet everything takes twice as long.”

Here are the pitfalls I see companies encounter all too often at this stage.

- Excessive churn: After $10M in ARR, churn often rears its ugly head for three main reasons:

- Overselling: Initially, all startups promise more than they can deliver. The successful ones build the features they’re promised before customers’ patience runs out. However, beyond $10M ARR, startups need to tamp down overselling to avoid dissatisfied customers who eventually churn, along with feature creep.

- Lack of processes: Many startups fail to establish the processes and teams needed to effectively onboard customers and support adoption. As a result, their products can’t be successfully implemented and, thus, can’t deliver value.

- ICP misalignment: In earlier phases, companies often experiment with their ICP and sign customers who aren’t good long-term fits. While ~10% logo churn is manageable (and perhaps up to 20% for SMB-focused products), anything higher risks a nosedive that’s difficult to pull out of.

- Accumulating tech debt: Every startup does things that don’t scale and “moves fast and breaks things.” Great engineering teams spin up new features overnight to get customers to sign on the dotted line. Yet, at some point, a major system redesign is inevitable. Timing this transition is critical. Do it too early and new feature development grinds to a halt. Wait too long and there is code sprawl, stalling forward progress and causing customer support tickets to overwhelm the team.

- Premature ICP expansion: Most startups expand their ICP in this phase, either going upmarket (to increase ACV) or downmarket (to shorten sales cycles and increase predictability). Many also expand into new verticals, find additional buying centers within organizations, and introduce new features and product lines to attract more users. These tactics are necessary to expand TAM and maintain growth. The key is to be intentional about these changes, sequence them appropriately, and make them at a pace that the organization can absorb.

Hold the center

In closing, when I reflect on the challenges that founders face as they fight their way to $100M in ARR, I’m reminded of a poem by William Butler Yeats that I read in high school. The first three lines read:

Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Escalating chaos, breakdowns in communication, a pervasive sense of unraveling: all of this mirrors the turmoil that founders encounter as their businesses scale.

For those that aspire to become more than just unicorns on paper, the key is to hold the center. Remain relentlessly focused on what matters—developing 10x better products and steadily building a resilient business around them—even as everything else roils.

Published on 01.31.2023

Written by Foundation Capital